Triple-Entry: The Future of Value

The conceptual architecture of modern finance is undergoing a fundamental transformation. For centuries, our representation of value has relied on descriptive, internal records that are vulnerable to manipulation and error. The arrival of Bitcoin marks a transition to an axiomatic, mathematically verifiable system known as triple-entry accounting. This report simplifies the history of record-keeping, explains the science behind triple-entry systems, and identifies Bitcoin as the definitive “Apex Asset” for proving global wealth and liquidity.

The Evolution of Bookkeeping: From Single to “Siloed” Double Entry

The history of accounting tracks humanity’s attempt to mitigate the erosion of trust and memory. Each technological leap in record-keeping has aimed to reduce the “gap” where fraud and error occur.

Single-Entry Bookkeeping (Ancient Era)

Used in Mesopotamia as early as 3500 BC, this method involved simple lists of assets and liabilities.[^1] It tracked “what is” (stocks) but lacked a mechanism for tracing “changes” (flows).[^1] In a single-entry system, a bad actor can simply remove a line from a ledger, and that asset effectively ceases to exist in the records, making it highly vulnerable to both error and intentional fraud.[^3]

Double-Entry Bookkeeping: The “Auditor Dilemma”

Codified by Luca Pacioli in 1494, double-entry bookkeeping introduced the “dual aspect concept,” governed by the equation:

\$\$ \text{Assets} = \text{Liabilities} + \text{Equity} \$\$

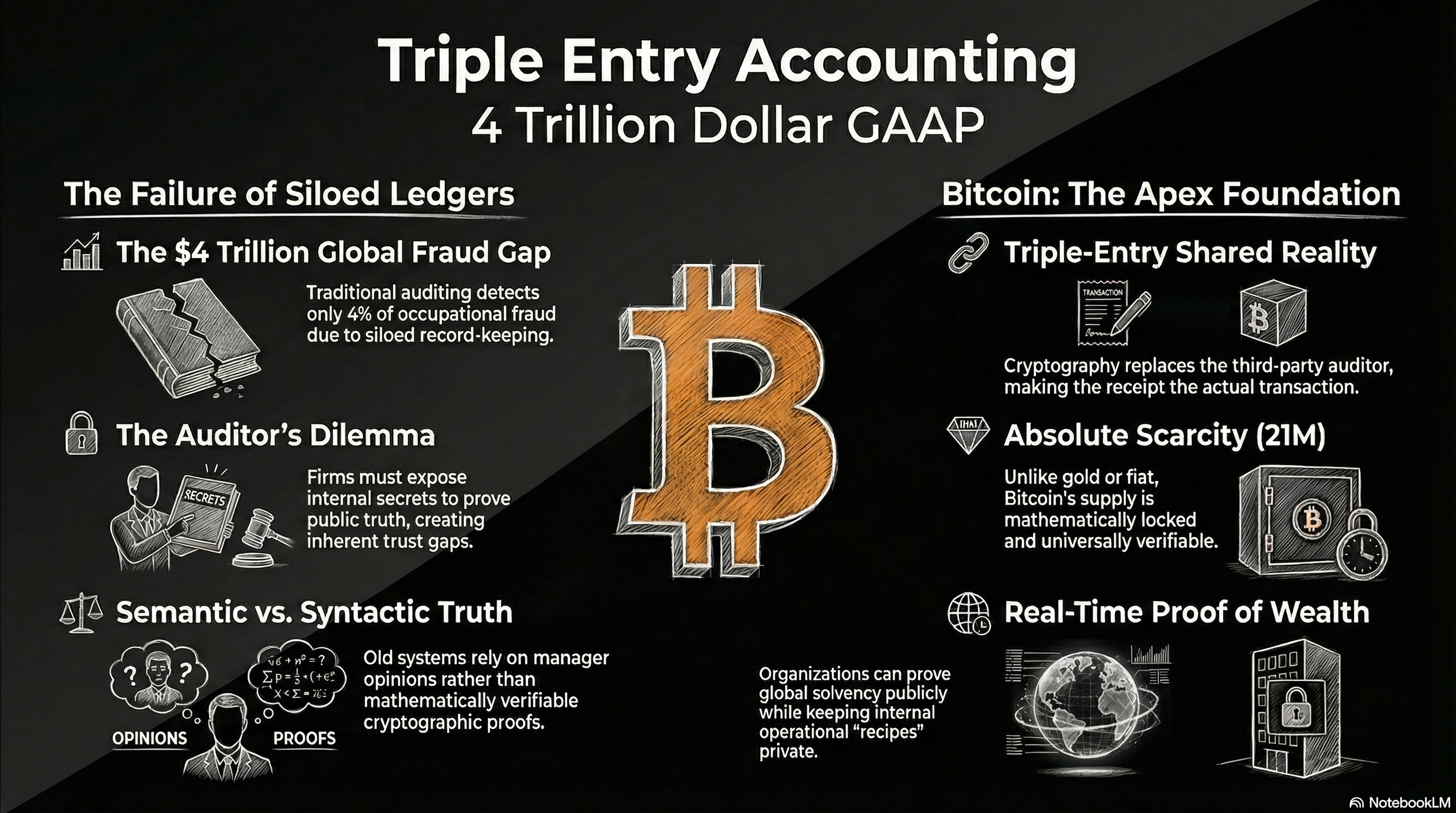

Every transaction is recorded twice—as a debit and a credit—ensuring internal equilibrium.[^5] While revolutionary for its time, double-entry is inherently siloed. Each firm maintains its own private ledger, creating a “disparate reality” where two parties to a transaction have two different sets of books.

This system is inherently prone to fraud because it relies on the “Auditor Dilemma”: an organization must expose its “Table Truth” (messy internal operations) to auditors to verify its “Public Truth” (curated financial statements). Traditional auditing is costly and insufficient, detecting only 4% of occupational fraud in 2017 while global fraud losses reached USD 4 trillion.[^1] The “truth” in double-entry is merely an internal opinion that requires expensive, periodic external reconciliation.

The Science of Triple-Entry Accounting: The Shared Truth

Triple-entry accounting (TEA) does not merely add a third column to a ledger; it introduces a cryptographic third party that turns private opinions into public facts.

The Griggian Model: The Signed Receipt

Popularized by Ian Grigg, the “third entry” is a digitally signed receipt shared between the two transacting parties and a dominant third party (the network).[^3]

- Party A (Payer): Signs a transaction request.

- Party B (Payee): Signs a transaction acceptance.

- The Network (Issuer/Ledger): Verifies the signatures, prevents double-spending, and timestamps the entry.

This creates a “bulletproof accounting layer” where The Receipt is the Transaction.[^9] There is no longer a need for post-hoc reconciliation because the entry on the shared ledger is the definitive reality, not a representation of it.[^3]

Syntactic vs. Semantic Truth

In traditional accounting, truth is semantic—it is based on what a manager says an asset is worth.[^7] In triple-entry, truth is syntactic—it is defined by the validity of the cryptographic proof. If a transaction satisfies the protocol’s mathematical consensus, it is true by definition.[^7]

Implementing Triple-Entry: The Bitcoin Paradigm Shift

Bitcoin is the first practical implementation of a triple-entry system, using math to create a “universally verifiable public truth.”

Bitcoin as Digital Capital: The Apex Asset

Bitcoin serves as the ultimate “Engine of Capital” due to its unique properties:

- Absolute Scarcity: Unlike gold, which has “pseudo-scarcity” (higher prices lead to more mining), Bitcoin has a mathematically locked 21 million unit cap.

- Real-Time Valuation: It provides perfect price discovery by trading 24/7 across global markets, unlike real estate or IP, whose values are theoretical until a sale occurs.

- Proof of Wealth: Organizations can exhibit their “cake” (stored wealth) on the blockchain for the whole world to see while keeping their “recipe” (operational secrets) private. This allows for friction-free capital exhibition and proves financial strength without revealing competitive advantages.

Lightning Channels: The Triple Accounting Backbone

We can envision a future financial architecture where corporations operate as high-speed layers above the base settlement layer:

- Private Working Capital (Money in Lightning): Corporations utilize Lightning Channels as a triple accounting backbone to handle high-frequency, B2B settlements off-chain.[^11] This “money” functions as private working capital, allowing for instant, near-zero-fee trade while maintaining operational privacy.

- Digital Capital (Treasury Bitcoin): The “wealth” of the organization is anchored in the Bitcoin base layer (L1). Bitcoin held in the corporate treasury serves as the definitive signal of liquidity and financial strength, which can be verified by the world in real-time.

Conclusion: The Convergence of Math and Value

The evolution from single to double-entry bookkeeping was a leap in error reduction, but it left a “trust gap” that necessitated human intermediaries. Triple-entry accounting closes this gap by moving truth from private ledgers to a shared mathematical protocol. By using Bitcoin as the base layer for digital capital and Lightning as the operational rail for private working capital, corporations can achieve a “Houdini-like” balance: proving absolute solvency to the world while maintaining complete privacy of their internal operations. This represents the final completion of the project begun by Pacioli, moving finance from the realm of “True and Fair” opinions to “Mathematically Valid” facts.

Tips and Donations

If you enjoyed this deep dive, consider supporting the project with a tip in Sats. It’s a simple, global way to support independent research.

To send Sats, you’ll need a lightning wallet.

References

- TRIPLE-ENTRY BOOKKEEPING A critical examination of an ostentatious accounting novelty, accessed March 30, 2026, https://www.rit.edu/croatia/sites/rit.edu.croatia/files/docs/2%20Schmidt%2C%20Vezjagi%C4%87.pdf

- Triple-Entry Bookkeeping - Bitcoin Magazine, accessed March 30, 2026, https://bitcoinmagazine.com/glossary/triple-entry-bookkeeping

- Triple Entry Accounting - MDPI, accessed March 30, 2026, https://www.mdpi.com/1911-8074/17/2/76

- stock flow consistent models - Critical Finance, accessed March 30, 2026, https://criticalfinance.org/tag/stock-flow-consistent-models/

- Double-Entry Accounting vs. Triple Entry Accounting In 2024 - BusActa Advisors, accessed March 30, 2026, https://busacta.com/double-entry-accounting-and-triple-entry-accounting/

- Commodity, Scarcity, and Monetary Value Theory in Light of Bitcoin, accessed March 30, 2026, https://nakamotoinstitute.org/library/commodity-scarcity-and-monetary-value-theory-in-light-of-bitcoin/

- (PDF) Triple‐entry accounting with blockchain: How far have we …, accessed March 30, 2026, https://www.researchgate.net/publication/336645713_Triple-entry_accounting_with_blockchain_How_far_have_we_come

- The Importance of (and challenges with) Valuing Intangibles, accessed March 30, 2026, https://ivsc.org/the-importance-of-and-challenges-with-valuing-intangibles/

- The Endogenous Constraint: Hysteresis, Stagflation, and the … - arXiv, accessed March 30, 2026, https://arxiv.org/html/2512.07886

- What is BTC? : r/Bitcoin - Reddit, accessed March 30, 2026, https://www.reddit.com/r/Bitcoin/comments/1na8jkk/what_is_btc/

- The DCF Valuation Methodology is Untestable, accessed March 30, 2026, https://corpgov.law.harvard.edu/2022/04/20/the-dcf-valuation-methodology-is-untestable/

- A LITERATURE REVIEW ON THE REPORTING OF INTANGIBLES - EFRAG, accessed March 30, 2026, https://www.efrag.org/sites/default/files/2023-11/A%20literature%20review%20on%20the%20reporting%20of%20intangibles.pdf