The Great Credit Pivot

The global credit landscape in early 2026 is undergoing a profound structural transformation, defined by a systemic divergence between traditional private lending markets and the burgeoning sector of digital-asset-linked corporate credit. As the1.2 trillion dollars private credit industry grapples with a surge in corporate bankruptcies, deteriorating borrower fundamentals, and increasingly restrictive redemption “gates” within flagship institutional funds, sophisticated capital is migrating toward more transparent, liquid, and high-yielding alternatives. Central to this transition is the Series A Perpetual Stretch Preferred Stock (STRC) issued by Strategy Inc., which has emerged as the premier fixed-income vehicle in the current macroeconomic environment. This report provides an exhaustive evaluation of the systemic stresses within the private credit market, analyzes the liquidity traps prevalent in legacy private equity-led funds, and argues that STRC represents a superior instrument based on its3.5% dividend, robust principal protection mechanisms tied to Bitcoin price floors, and a tax-efficient Return of Capital (ROC) structure that delivers a taxable-equivalent yield nearing 20%.

The State of Global Credit: Bankruptcy Resurgence and the Private Debt Cycle

The year 2025 served as a reckoning for the private credit market, which had expanded with reckless abandon from 54 billion dollars in 205 to a staggering1.6 trillion dollars by early 2025. Entering 2026, the industry is facing its first comprehensive test of a full credit cycle, and the results indicate a market on a “hair trigger”. Corporate bankruptcies in the United States reached their highest pace since 207, marking a sharp rise that reflects mounting financial pressure on businesses struggling to manage high interest burdens and trade policy uncertainties. The fragility of the current environment is evidenced by the “true” default rate in private credit, which, when adjusted for out-of-court restructurings and liability management exercises, is estimated to be approaching 5%. This is significantly higher than the headline default rates typically reported by fund managers, which often mask distress through selective defaults and consensual debt-for-equity exchanges.

Borrower Fundamentals and the PIK Debt Trap

A critical driver of this distress is the deteriorating cash flow of corporate borrowers. Data from the International Monetary Fund’s 2025 Financial Stability Report indicates that approximately 40% of private credit borrowers now have negative free cash flow, a dramatic increase from 25% just four years ago. This cash flow deficit has forced a widespread reliance on Payment-In-Kind (PIK) interest toggles. PIK usage, once a niche feature of mezzanine debt, has now permeated senior secured loan documentation, with public Business Development Companies (BDCs) now receiving an average of 8% of their investment income via PIK. This “PIK trap” creates a dangerous feedback loop: borrowers defer cash interest payments by increasing their total debt load, which ostensibly preserves the fund’s internal rate of return (IRR) on paper but starves the fund of actual cash distributions (DPI). Consequently, investors are increasingly adopting the mantra that “DPI is the new IRR,” prioritizing realized cash distributions over the subjective and potentially inflated valuations provided by private fund managers.

| Market Stress Indicator | 2021/2022 Benchmark | 2025/2026 Current Level | Systemic Implication |

|---|---|---|---|

| Borrowers with Negative Free Cash Flow | 25% | 40% | High insolvency risk in mid-market |

| BDC Income from PIK Interest | < 4% | 8% | Interest coverage is failing |

| Adjusted Private Credit Default Rate | ~2% | ~5% | Hidden decay in asset quality |

| Annual Business Bankruptcies | ~18,04 | > 19,84 | Highest activity since post-202 |

The Impact of AI and Trade Volatility

Adding to the fundamental distress is the disruption caused by artificial intelligence and shifting trade policies. Retailers and consumer brands, already vulnerable to weaker demand, are facing margin erosion as they fail to adapt to AI-driven logistics and consumer shifts. Furthermore, the “Liberation Day” tariff announcements in April 2025 created a shock to industrial supply chains, leading to a wave of distressed situations that opportunistic credit funds are now scrambling to capitalize on. This environment has exposed the limitations of traditional “clubby” lending structures, which often lack the flexibility to address rapid technological and regulatory shifts.

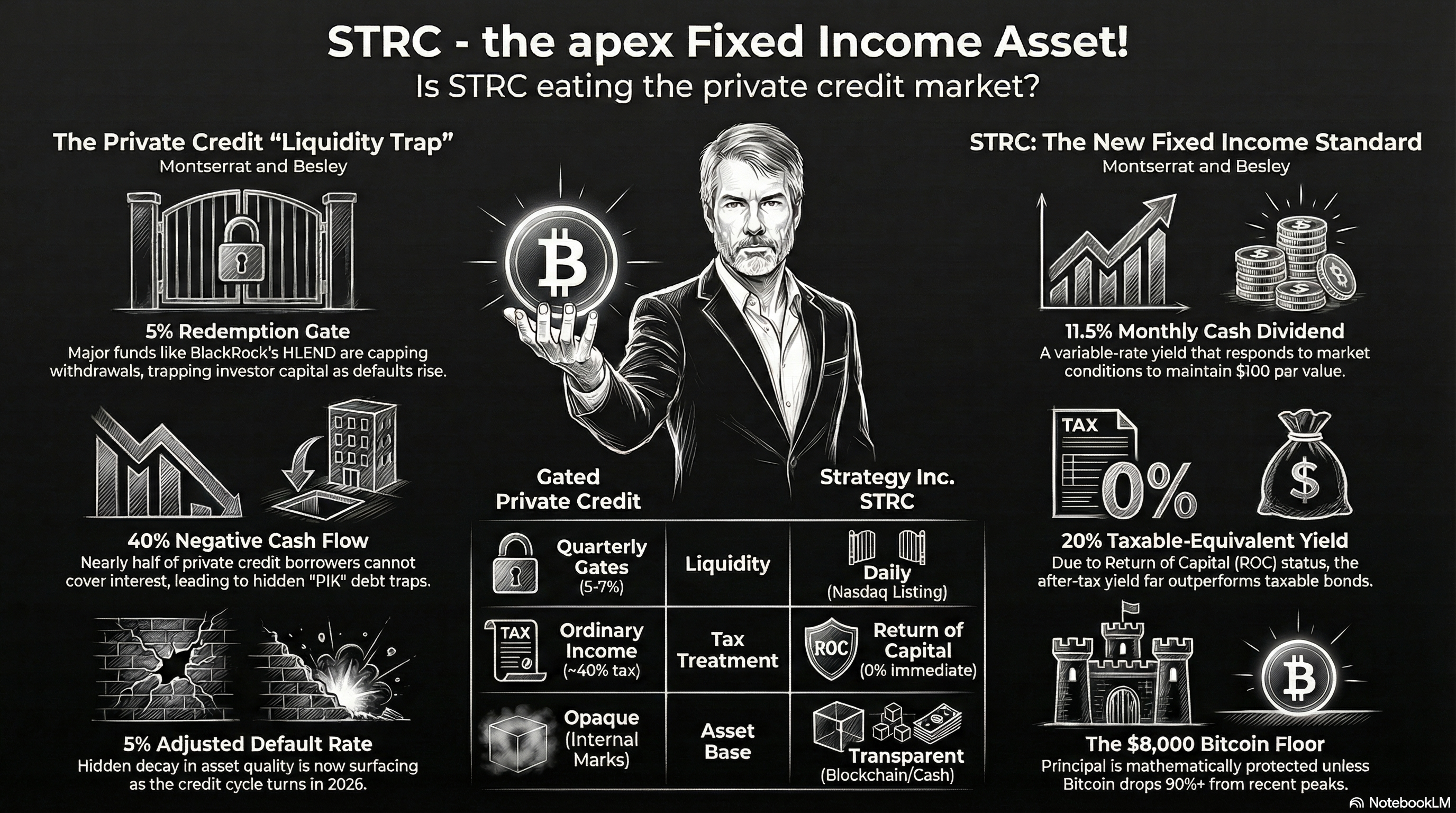

The Redemption Trap: Liquidity Gating at BlackRock and Blackstone

As corporate credit quality deteriorates, retail and institutional investors have sought to rebalance their portfolios, only to find that the liquidity promised by many “evergreen” and “semi-liquid” private credit funds is illusory. The first quarter of 2026 saw a record wave of redemption requests that tested the structural limits of the industry’s largest players.

BlackRock’s HLEND: The 5% Barrier

BlackRock’s 26 billion dollars HPS Corporate Lending Fund (HLEND) [2], one of the most prominent non-traded BDCs, provided a stark example of “gated” liquidity in March 2026. Following a spike in retail anxiety, shareholders requested redemptions for10.3% of the fund’s outstanding shares. However, BlackRock management exercised its right to cap repurchases at just 5% of the fund’s value, effectively trapping nearly half of the requested capital. This move, while legal and consistent with the fund’s design, highlights the fundamental mismatch between the liquid expectations of investors and the illiquid nature of the underlying private loans. For many investors, the realization that they cannot access their principal during a period of perceived market stress has eroded the “peace of mind” that these semi-liquid vehicles were designed to provide.

Blackstone’s BCRED: A Strained Threshold

Similarly, Blackstone’s flaghip 82 billion dollars Private Credit Fund (BCRED) [16, 14] faced a liquidity test in early 2026. Redemption requests reached11.9% of the fund’s value, exceeding its standard 5% quarterly limit. To prevent a total freeze, Blackstone was forced to raise the redemption cap to 7% and coordinate a 44 million dollars capital injection from its own senior leaders and employees to help satisfy withdrawal requests. While this successfully managed the immediate crisis, the net outflow of1.11 billion dollars for the quarter signaled a significant shift in investor sentiment. These incidents at BlackRock and Blackstone demonstrate that when “bankruptcies loom large,” the redemption limits of private equity-led funds become a primary risk factor for investors. The opacity of these funds’ internal valuations (marks) further complicates the issue, as investors fear they may be redeeming at prices that do not reflect the true market value of the distressed loans held in the portfolio.

Strategy Inc. and the New Paradigm of Digital Credit

In direct contrast to the opaque and gated world of private credit, Strategy Inc. has engineered a transparent, high-yield credit mechanism that leverages its position as the world’s largest Bitcoin treasury company. Holding approximately 75,737 Bitcoins as of March 2026, the company has pivoted from common equity issuance toward a sophisticated preferred capital structure designed to attract fixed-income investors.

The Rise of STRC: The “Stretch” Preferred Perpetual

The cornerstone of this new digital credit standard is the Variable Rate Series A Perpetual Stretch Preferred Stock (STRC). Since its IPO in July 2025 [4], STRC has rapidly become the most successful preferred security in the market from a volume standpoint, even though it is less than a year old. In 2025 alone, STRC and its sister preferred securities accounted for 33% of the entire U.S. preferred market issuance, raising11 billion dollars in capital. STRC is designed to offer a “Short Duration High Yield Credit” profile. Listed on the Nasdaq, it provides the “absolute openness” that private credit funds lack—offering daily liquidity and transparent market pricing. The stock has a 14 dollars par value, and its dividend rate is adjusted monthly by the board to ensure it trades near this par value, effectively stripping away the price volatility typically associated with high-yield crypto-related assets.

The3.5% Monthly Variable Dividend

As of March 2026, the annual dividend rate for STRC was raised to3.50% [5, 17], payable monthly in cash. This was the seventh consecutive monthly hike, moving up from3.25% in February. This variable rate mechanism is a cornerstone of the STRC value proposition; it allows the company to respond to market volatility in real-time. If the stock begins to trade below par, the board can increase the yield to attract buyers, thereby anchoring the trading price near 14 dollars. This monthly reset provides a “digital yield curve” that is far more responsive than the quarterly or semi-annual distribution schedules of traditional BDCs or preferred stocks. For income-focused investors, the3.5% yield represents a significant premium over the2.0% to2.5% yields expected from senior secured private credit loans in 2026.

Argue for STRC: The Best Fixed Income Vehicle on the Market

The superiority of STRC over traditional fixed-income instruments and gated private credit funds is established through three primary pillars: absolute principal protection floors, dividend security through massive cash reserves, and superior after-tax yields.

Pillar I: Principal Protection and the2,04 dollars Bitcoin Floor

The defining characteristic of STRC is the “mathematical moat” provided by Strategy Inc.’s Bitcoin treasury. While STRC is not directly collateralized by the Bitcoin (holders have a preferred claim on residual assets), the asset coverage is so extensive that it provides a theoretical principal floor that is unmatched in the corporate bond market. As of early 2026, Strategy Inc. holds over 75,04 Bitcoins, acquired for an aggregate cost of 54.77 billion dollars. Against this massive asset base, the company has layered a capital stack that includes approximately2.25 billion dollars in debt and2.47 billion dollars in preferred stock notional value. The logic of the “8,04 dollars Bitcoin floor” is derived from a simple solvency calculation. For the company to be unable to satisfy the principal value of its preferred stock, the value of its Bitcoin would have to drop to a point where it could not cover both the senior debt and the preferred equity. At2,04 dollars per Bitcoin, the company’s 75,737 coins would still be worth approximately8.76 billion dollars. When combined with the12.25 billion dollars to12.8 billion dollars U.S. dollar cash reserve, the total liquid assets would be roughly2 billion dollars to2.25 billion dollars. This provides a massive buffer; Bitcoin would have to experience a catastrophic, 90%+ decline from its late-2024 peaks before the principal of STRC is even theoretically impaired. Compared to a traditional corporate bond, where principal is tied to the survival of a company with negative free cash flow, STRC offers “sovereign-grade” asset coverage.

Pillar II: Dividend Security through the12.8 billion dollars Cash Pile

A common risk in high-yield instruments is the “distribution holiday,” where a company suspends dividends to preserve cash. Strategy Inc. has pre-emptively mitigated this risk by establishing a massive U.S. dollar reserve. The company’s 2026 annual report [7] details a12.25 billion dollars (growing toward12.8 billion dollars) cash and cash equivalents reserve specifically earmarked to support preferred dividends and interest payments. This cash pile ensures that even in a prolonged “crypto winter” where Strategy Inc. chooses not to sell its Bitcoin, it can continue to honor its3.5% dividend for years without needing to tap into its digital assets or issue new equity. This stands in stark contrast to private credit funds, which rely on the monthly cash flow of their underlying borrowers—40% of whom are currently cash-flow negative—to fund investor payouts.

Pillar III: The ROC Tax Advantage and the 20% Taxable Equivalent

Perhaps the most compelling argument for STRC is its tax efficiency. Strategy Inc. expects that its preferred dividends will be treated as a non-taxable Return of Capital (ROC) for U.S. federal income tax purposes. Under IRC Section 301(c) [22], an ROC distribution is not considered taxable income in the year received; instead, it reduces the investor’s tax basis in the security. Taxes are only paid upon the sale of the security, typically at the lower long-term capital gains rate, or potentially avoided entirely through “step-up” basis rules upon inheritance. To put STRC on an equal footing with a taxable bond, we use the Taxable-Equivalent Yield (TEY) formula: For a high-net-worth investor in the 40.8% combined federal tax bracket (37% top rate + 3.8% Net Investment Income Tax) : When accounting for state taxes and the time-value of tax deferral, the “real” yield of STRC is effectively par with a 20% taxed yield. In the current market, where the average high-yield corporate bond yields less than 9% pre-tax, the after-tax superiority of STRC is mathematically undeniable.

| Metric | Gated Private Credit Fund | Strategy Inc. STRC Preferred |

|---|---|---|

| Nominal Yield | ~9.7% | 11.50% |

| Tax Treatment | Ordinary Income (~44.8% tax) | Return of Capital (0% Immediate tax) |

| Liquidity | Quarterly Gates (5-7%) | Daily (Nasdaq) |

| Asset Transparency | Opaque (Internal Marks) | Real-time (Bitcoin/Blockchain) |

| Taxable Equivalent Yield | ~9.7% | ~20% |

Market Volume and Investor Migration: The “Openness” Premium

The success of STRC is most clearly visible in its trading volume. Despite being only six months old, it has achieved an average daily trading volume (ADV) of over1.11 million shares, closing in on the liquidity levels of established preferred ETFs like the iShares Preferred & Income Securities ETF (PFF). Investors are not just leaving private equity and private credit because of the high yield; they are fleeing the “clubby,” opaque nature of those instruments in favor of a security that is “absolutely open”. STRC represents a democratization of high-yield credit. It allows investors to participate in a sophisticated “Bitcoin-backed yield curve” with the same ease as buying a share of Apple or Amazon. The inclusion of STRC as a top-five holding in major institutional ETFs like PFF (at a1.48% weighting) signals that the professional community has accepted it as a core component of the modern fixed-income landscape. The “flywheel” effect—whereby STRC proceeds buy Bitcoin, which increases asset coverage, which lowers risk and attracts more STRC buyers—has created a reflexive growth model that traditional private credit cannot replicate.

Conclusion: Why STRC is the Ultimate Fixed Income Standard

The convergence of looming corporate bankruptcies, the structural failures of “semi-liquid” private credit funds, and the innovative engineering of Strategy Inc. has created a “perfect storm” that favors the ascent of digital-linked credit. The traditional private equity model of “gated” redemptions and opaque internal valuations is increasingly seen as a relic of a low-interest-rate era that has now passed. As argued throughout this report, STRC is the most successful preferred stock from a volume standpoint because it solves the fundamental issues of the current credit cycle. It provides:

- Yield: An3.5% monthly dividend that responds to market conditions.12. Protection: A principal “floor” backed by 75,000+ Bitcoins, resilient down to an2,04 dollars floor.6. Liquidity: A dedicated12.8 billion dollars cash pile to ensure continuous payouts and a Nasdaq listing for instant exit.13. Tax Alpha: An ROC treatment that elevates its “real” yield to nearly 20% for high-net-worth holders.

The migration of capital from private equity and gated BDCs into STRC is not a temporary trend; it is a fundamental shift toward “Open Credit.” Investors are choosing Strategy Inc. because it offers a transparent, liquid, and mathematically superior way to capture high yields without the existential risks of opaque borrowers and restrictive fund managers. In the final analysis, STRC is not merely a “crypto” product; it is the final arbiter of value in a market that has rediscovered the importance of liquidity and asset coverage.

Tips and Donations

If you enjoyed this deep dive, consider supporting the project with a tip in Sats. It’s a simple, global way to support independent research.

To send Sats, you’ll need a lightning wallet.

References

-

Private Credit Outlook 2026: The Market Faces its First Big Test - With Intelligence [1], https://www.withintelligence.com/insights/private-credit-outlook-2026/ ↩ ↩2 ↩3 ↩4 ↩5 ↩6

-

The Rise of Private Credit: 2026 Market Trends and Growth Outlook - Creative Planning, https://creativeplanning.com/insights/high-net-worth/rising-popularity-private-credit/ ↩ ↩2 ↩3 ↩4 ↩5 ↩6 ↩7 ↩8 ↩9 ↩10 ↩11

-

A Test of Endurance: 2025 Private Credit Restructuring Year in Review - Proskauer, https://www.proskauer.com/report/a-test-of-endurance-2025-private-credit-restructuring-year-in-review ↩ ↩2 ↩3 ↩4 ↩5 ↩6 ↩7

-

Earnings call transcript: MicroStrategy’s Q2 2025 beats expectations, stock rises, https://www.investing.com/news/transcripts/earnings-call-transcript-microstrategys-q2-2025-beats-expectations-stock-rises-93CH-4164706 ↩ ↩2 ↩3 ↩4 ↩5 ↩6 ↩7 ↩8 ↩9 ↩10 ↩11 ↩12

-

Clawd Bot : not another #AI chat thing ! by Deep Dive with Gemini - Spotify for Creators, https://creators.spotify.com/pod/profile/deepdivewithgemini/episodes/Clawd-Bot–not-another-AI-chat-thing-e3e8bjj ↩ ↩2 ↩3 ↩4 ↩5

-

Outlook for Private Credit in 2026 | Cleary M&A and Corporate Watch, https://www.clearymawatch.com/2026/02/outlook-for-private-credit-in-2026/ ↩ ↩2 ↩3

-

2025 Bankruptcy Roundup: Rising Filings and Evolving Dynamics - Mintz, https://www.mintz.com/insights-center/viewpoints/2831/2026-01-15-_025-bankruptcy-roundup-rising-filings-and-evolving ↩

-

Strategy Increases STRC Dividend to 11.50% - BitcoinTreasuries.NET, https://bitcointreasuries.net/news/strategy-increases-strc-dividend-to-1150percent ↩ ↩2 ↩3 ↩4 ↩5 ↩6

-

Strategy Inc boosts bitcoin and raises STRC dividend | MSTR SEC …, https://www.stocktitan.net/sec-filings/MSTR/8-k-strategy-inc-reports-material-event-0df660f4f219.html ↩

-

Wall Street Warns About a Possible Private Credit Collapse. Should Investors Worry About These Ultra-High-Yield Stocks? | The Motley Fool, https://www.fool.com/investing/2026/02/02/wall-street-warns-about-a-possible-private-credit/ ↩

-

Massive bitcoin stack defines Strategy Inc (MSTR) 2025 annual report - Stock Titan, https://www.stocktitan.net/sec-filings/MSTR/10-k-strategy-inc-files-annual-report-9656434d4cfd.html ↩ ↩2 ↩3 ↩4

-

BlackRock’s 26 billion dollars private credit fund limits withdrawals …, https://www.businesstimes.com.sg/wealth/wealth-investing/blackrocks-us26-billion-private-credit-fund-limits-withdrawals ↩ ↩2 ↩3 ↩4 ↩5 ↩6 ↩7

-

STRC Information - Strategy, https://www.strategy.com/stretch ↩