The Battle for Your 401k

Date: December 11, 2025 Subject: The Legislative and Regulatory Conflict Over Digital Assets in Defined Contribution Plans

Abstract

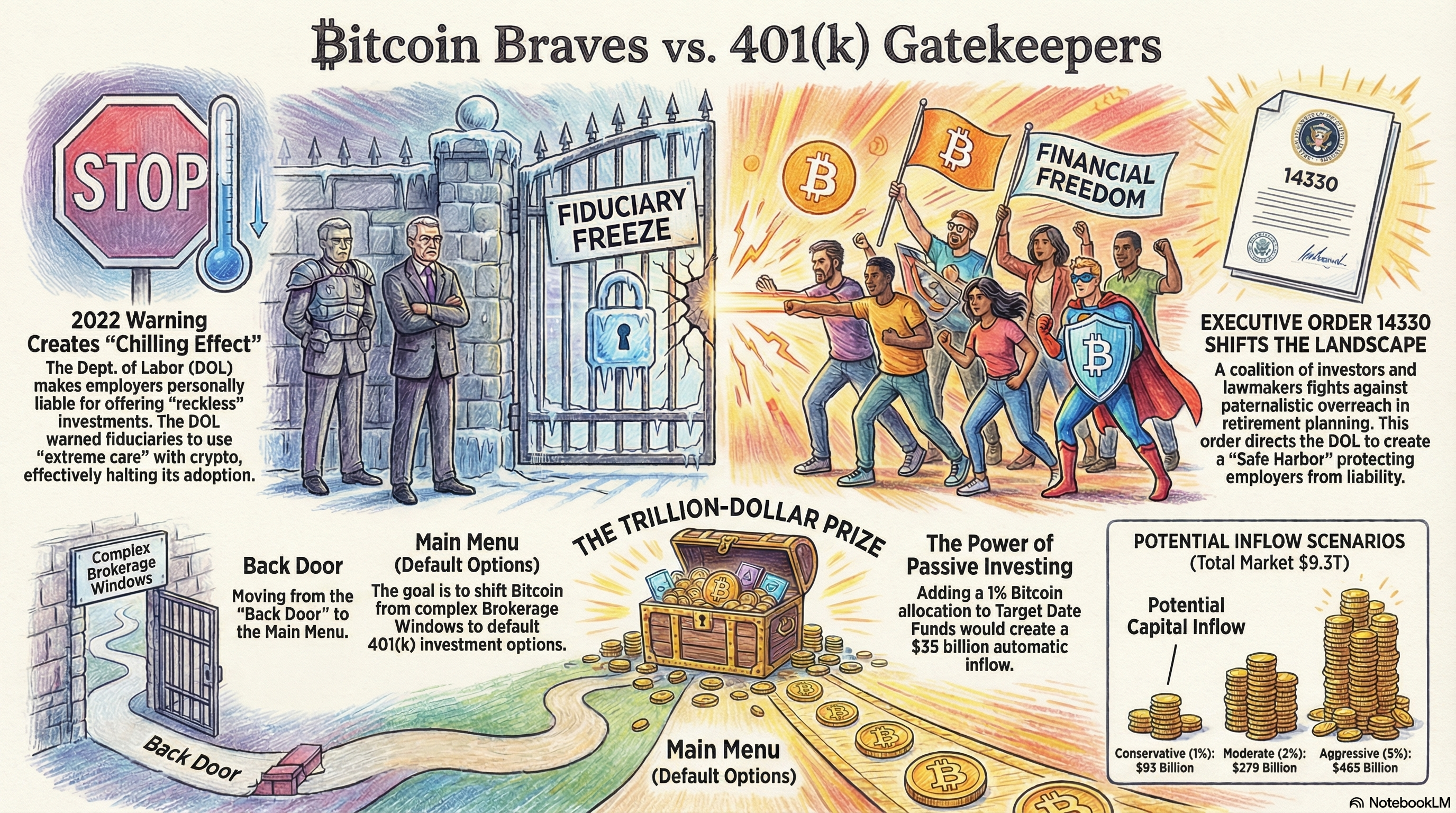

As of late 2025, the U.S. retirement market holds approximately USD 9.3 trillion in 401(k) assets. Yet, despite the widespread adoption of Bitcoin ETFs in personal brokerage accounts, nearly 0% of this capital is allocated to digital assets within standard “Core Menus.” This paper examines the conflict between the “Gatekeepers”—federal regulators and risk-averse plan fiduciaries—and the “Bitcoin Braves”—a coalition of retail investors and congressional leaders pushing for access. It analyzes the pivotal impact of Executive Order 14330 and the Retirement Investment Choice Act in dismantling the “fiduciary freeze” that has historically blocked Bitcoin from the world’s largest capital pool.

I. The Gatekeepers: The Fiduciary Freeze

For decades, the primary gatekeepers of the American 401(k) have been the Department of Labor (DOL) and the Employee Benefits Security Administration (EBSA). Their mandate is to enforce the Employee Retirement Income Security Act of 1974 (ERISA), specifically the “prudent man rule,” which holds employers personally liable if they offer reckless investment options to employees.

The “Chilling Effect” of 2022

The conflict stems largely from Compliance Assistance Release No. 2022-01, issued by the DOL in March 2022. This guidance warned plan fiduciaries to exercise “extreme care” before adding cryptocurrencies to 401(k) investment menus, explicitly threatening investigation programs for plans that did so [1].

- The Result: While not an explicit ban, this created a “regulatory freeze.” Fiduciaries (employers) operate on a basis of liability minimization. Even after the approval of Bitcoin ETFs in 2024 made the asset class regulated and securitized, the fear of DOL litigation kept Bitcoin off the “Core Menu” of major recordkeepers like Vanguard and Fidelity.

II. The Bitcoin Braves: The Push for “Financial Freedom”

Against this “freeze,” a coalition of “Bitcoin Braves” emerged, driven by both ideological and economic incentives. This group includes retail investor organizations like the Financial Choice Coalition and key lawmakers who viewed Bitcoin as the ultimate protection against inflation.

The “Self-Directed” Loophole

Between 2022 and 2024, the only way for 401(k) participants to access Bitcoin was through Self-Directed Brokerage Accounts (SDBAs) or “windows.” Unlike the “Core Menu” selected by the employer, an SDBA allowed employees to choose their own stocks and ETFs.

- Fidelity’s Digital Assets Account: In late 2022, Fidelity became the first major recordkeeper to allow employers to offer a 20% Bitcoin allocation within their plan. However, usage remained low due to the immense pressure from the DOL.

III. The Breakthrough: The Retirement Investment Choice Act (2025)

The legal stalemate broke in early 2025 with the passage of the Retirement Investment Choice Act. This legislation specifically amended ERISA to clarify that the inclusion of SEC-regulated spot Bitcoin ETFs in a 401(k) menu does not, by itself, constitute a breach of fiduciary duty.

Key Provisions:

- Liability Protection: It created a “Safe Harbor” for employers who offer diversified, regulated digital asset ETFs.

- No “Merit Regulation”: It prohibited the DOL from using “merit regulation” to single out digital assets as inherently riskier than traditional equities or junk bonds.

- Default Investment Rights: It paved the way for the first Bitcoin-inclusive Target Date Funds (TDFs).

IV. Conclusion: The 9 USD Trillion Tsunami

By late 2025, the transition began. The “fiduciary freeze” thawed as recordkeepers moved to integrate Bitcoin ETFs into their standard platforms. While initial allocations remain conservative (typically 1–3%), the sheer scale of the 401(k) market means that even a 1% shift represents 90 billion USD in new demand.

The battle for the 401(k) was never just about a single asset; it was a battle over the definition of “Prudence” in an era of digital scarcity. As the Braves dismantled the barriers of the Gatekeepers, they didn’t just add a ticker symbol to a menu; they secured the right for millions of Americans to allocate their long-term savings to the hardest money ever created.

Tips and Donations

If you enjoyed this deep dive, consider supporting the project with a tip in Sats. It’s a simple, global way to support independent research.

To send Sats, you’ll need a lightning wallet.

References

[1]: Department of Labor (DOL). (2022). Compliance Assistance Release No. 2022-01: 401(k) Plan Investments in Cryptocurrencies. [2]: U.S. Congress. (2025). The Retirement Investment Choice Act: Amending ERISA for the 21st Century. [3]: Fidelity Digital Assets. (2024). Digital Assets in Retirement Plans: 2024 Institutional Report.