Hacking Your Retirement

1. Introduction: The Concept of the “California Free Lunch”

The state of California presents a paradox of wealth and affordability. It stands as the world’s fifth-largest economy, a crucible of technological innovation and real estate appreciation, yet it imposes some of the highest costs of living and tax burdens in the United States. For the high-net-worth individual or the middle-class family sitting on significant unrealized real estate equity, the “California Dream” often devolves into a cash-flow struggle—asset rich, but liquidity constrained by property taxes, insurance premiums, and the general cost of shelter.

This research report evaluates a specific, highly sophisticated financial arbitrage strategy designed to invert this dynamic. The theoretical case study posits a radical restructuring of a household’s balance sheet: the liquidation of a primary residence to harvest tax-free capital gains under Internal Revenue Code Section 121; the redeployment of that capital into a high-yield, aggressive corporate preferred security (Strategy Inc., ticker STRC) structured to return capital rather than taxable income; the utilization of the Modified Adjusted Gross Income (MAGI) accounting methodology to qualify for state-subsidized healthcare (Medi-Cal); and the transition from homeownership to tenancy in specific, high-value rental markets.

This strategy is not merely a financial plan; it is a regulatory arbitrage that exploits the disconnect between wealth (asset ownership) and income (taxable recognition). It operates in the gray zones between federal tax law, state social welfare policy, and corporate financial engineering. This analysis will deconstruct the mechanics, viability, and existential risks of this approach, utilizing a 2026 forward-looking perspective that incorporates the reinstatement of Medi-Cal asset tests, the credit profile of Bitcoin-linked corporate treasuries, and the realities of the California housing market.

2. The Capital Preservation Phase: Optimizing Section 121

The foundational capital for this strategy is derived from the conversion of illiquid real estate equity into deployable cash. In the California market, where long-term appreciation has historically outpaced the national average, the accumulated equity in a primary residence often represents the bulk of a household’s net worth.

2.1 The Mechanics of IRC Section 121

Internal Revenue Code Section 121 provides one of the few remaining tax shelters available to the middle and upper-middle class. It allows a taxpayer to exclude up to USD 250,02 of gain from the sale of a principal residence from gross income. For married couples filing jointly, this exclusion doubles to USD 52,02.1

To qualify for this exclusion, the taxpayer must meet the “ownership and use” tests: they must have owned and used the home as their principal residence for at least two of the five years immediately preceding the sale. Importantly, this exclusion is renewable; it can be claimed once every two years.

In the context of the “California Arbitrage,” Section 121 is not just a tax deduction; it is a capital preservation engine. For a California homeowner with USD 52,02 in capital gains, the tax liability without this exclusion would be substantial. Federal long-term capital gains tax rates for 2026 are projected to be 15% for most filers, rising to 20% for taxable incomes over USD 63,72 for married couples.1

Furthermore, high-income earners are subject to the Net Investment Income Tax (NIIT) of4.8%.4 Crucially, California does not offer a preferential tax rate for capital gains; they are taxed as ordinary income, with rates climbing as high as3.3% (or5.4% for earners over USD1 million including the mental health services tax).

Therefore, a non-exempt realization of USD 52,02 in gains could trigger a combined tax liability approaching 33-37% (Federal + State + NIIT), erasing nearly USD 165,02 to USD 185,02 of purchasing power. By utilizing Section 121, the household retains 100% of this equity. This preservation of principal is essential, as the subsequent income-generation strategy relies on a maximized capital base to generate sufficient yield to cover living expenses.6

2.7 Liquidation vs. Retention

The decision to sell implies a shift from “housing as a consumption good and inflation hedge” to “housing as a service.” Retaining the home involves “sunk costs” that are often invisible to the owner:

- Property Taxes: Under California’s Proposition3, taxes are generally limited to 1% of the assessed value plus local bonds, with increases capped at 2% annually. However, for long-term holders, the tax base is low. For recent buyers, it is substantial.

- Maintenance: Generally estimated at1 percent of the property value annually.

- Insurance: California’s insurance market is in crisis, with premiums for fire and casualty coverage escalating rapidly.

- Opportunity Cost: The equity trapped in the walls of the home earns 0% yield.

By liquidating, the household converts an asset yielding 0% (and costing ~1-2% annually to maintain) into an asset yielding nominally 11% (Strategy Inc. Preferred). The arbitrage lies in the spread between the investment yield and the cost of renting equivalent shelter. For example, a USD1.7 million home, if converted to liquid capital, can generate significant income. The capital of USD1.7 million invested at 5% risk-free equals USD 60,000/year (USD8,000/mo).

3. The Income Engine: Strategy Inc. (STRC) and the Bitcoin Treasury

The viability of living “free” depends on generating a massive stream of cash flow that is largely invisible to the tax authorities. The vehicle selected for this case study is the preferred equity of Strategy Inc., formerly known as MicroStrategy.

3.1 Corporate Identity and Strategic Shift

Strategy Inc. presents a unique corporate profile. Originally an enterprise analytics software company, it pivoted aggressively under Executive Chairman Michael Saylor to become a “Bitcoin Treasury Company”.8 The company leverages its balance sheet to acquire Bitcoin, issuing debt and equity to fund these purchases. As of late 2025/early 2026, the company held over 650,02 Bitcoins, making it the largest corporate holder of the asset in the world.9

The rebranding from MicroStrategy to Strategy Inc. in 2025 signaled a formalization of this dual-entity structure: a stable, cash-flow-positive software business effectively subsidizing a massive, leveraged Bitcoin hedge fund.10

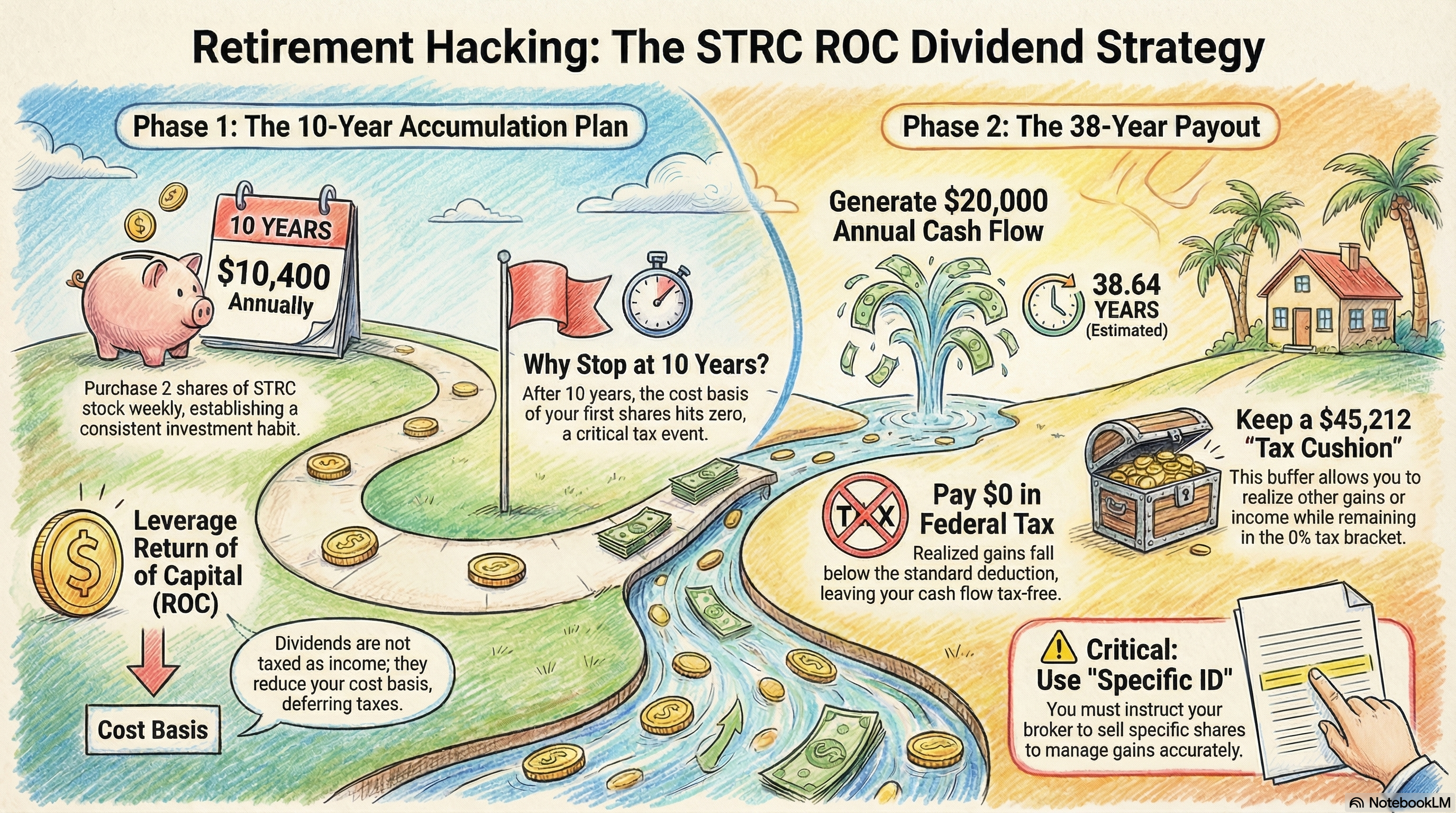

3.7 The STRC Instrument Analysis

The “Variable Rate Series A Perpetual Stretch Preferred Stock” (Ticker: STRC) is the specific instrument chosen for this strategy. It is a sophisticated hybrid security designed to appeal to yield-hungry investors while providing the issuer with flexible capital.4.7.1 Dividend Mechanics and Yield

The “Stretch” preferred stock has a par value of USD 12. Its defining feature is a variable dividend rate that is adjusted monthly. The company’s board of directors reviews the trading price of the stock relative to its USD 12 par value. If the stock trades at a premium (above USD 100), the dividend rate may be lowered to cool demand. Conversely, if it trades at a discount (below USD 100), the rate is increased to support the price.11

As of January 2026, Strategy Inc. announced an increase in the annual dividend rate to12.00%, payable monthly.13 For an investor deploying USD1,02,02 (the hypothetical proceeds from the home sale), this instrument generates USD 114,02 annually, or approximately USD13,166 per month.

This 11% nominal yield is significantly higher than the prevailing risk-free rate or investment-grade corporate bond yields, reflecting the substantial credit risk associated with the issuer.4.7.7 Tax Characterization: Return of Capital (ROC)

The “secret sauce” of this strategy is the tax treatment of the STRC distributions. In the United States, corporate distributions are taxed as dividends only if the corporation has “Earnings and Profits” (E&P), a specific tax accounting metric.

Strategy Inc.’s business model involves massive capital expenditures on Bitcoin and the issuance of convertible debt. Even with the adoption of fair value accounting for digital assets, the company frequently reports tax losses or minimal E&P due to the mechanics of its treasury operations and software business overhead.12

When a corporation distributes cash in excess of its E&P, the distribution is characterized as a Return of Capital (ROC).

- Non-Taxable: ROC is not considered taxable income in the year it is received. Instead, it is treated as a return of the investor’s original investment.15

- Basis Reduction: The investor must lower their “cost basis” in the stock by the amount of the ROC distribution.

- Capital Gains Deferral: Tax is deferred until the cost basis is reduced to zero. Once the basis hits zero, any further distributions are taxed as long-term capital gains (assuming the stock has been held for more than a year).3

For the “living free” strategist, this is critical: a USD 114,02 annual cash flow from STRC, if fully characterized as ROC, results in USD2 of reportable taxable income on the first page of the Form 1040. It does not flow into Adjusted Gross Income (AGI).

3.4 Credit Profile and Solvency Risks

The allure of an 11% tax-deferred yield must be weighed against the solvency of the issuer. Strategy Inc. is not a risk-free borrower.4.4.1 S&P Credit Rating

In October 2025, S&P Global Ratings assigned Strategy Inc. a ‘B-’ issuer credit rating with a stable outlook.8 In the parlance of credit markets, this is “junk” status, specifically “highly speculative.”

- Rationale: S&P cited the company’s “narrow business focus,” “weak risk-adjusted capitalization,” and “low U.S. dollar liquidity” as key weaknesses. Crucially, S&P’s methodology deducts Bitcoin holdings from equity when calculating risk-adjusted capital (RAC), resulting in a view that the company has “negative total adjusted capital”.8

- Implication: The rating agency views the Bitcoin holdings not as a stabilizer, but as a source of extreme volatility that could impair the company’s ability to meet its obligations.4.4.7 The Bitcoin Correlation

The STRC dividend is paid in U.S. dollars, but the company’s assets are primarily Bitcoin. This creates a currency mismatch. Debt maturities, interest, and preferred dividends are USD obligations. If Bitcoin were to suffer a catastrophic and sustained devaluation (a “crypto winter”), Strategy Inc.’s ability to raise USD liquidity (by selling Bitcoin or issuing new equity) could be severely compromised.8 While the software business provides some cash flow, it is insufficient to cover the massive capital structure obligations alone.4.4.4 Subordination

The STRC preferred stock sits low in the capital stack. It is junior to all indebtedness, including the billions in convertible notes Strategy Inc. has issued. In a bankruptcy or liquidation scenario, STRC holders would likely be wiped out completely, receiving zero recovery after bondholders are paid.11

4. The Regulatory Interface: Medi-Cal Eligibility

The second pillar of the “Live Free” strategy is the elimination of healthcare costs. In the United States, healthcare is a major line item for early retirees. California’s Medicaid program, Medi-Cal, offers a solution, but its eligibility rules are a labyrinth of age-based and income-based criteria that are undergoing a seismic shift in 2026.

4.1 The MAGI Framework (Under Age 65)

For individuals between the ages of16 and 64 who are not eligible for Medicare, Medi-Cal eligibility is determined exclusively by Modified Adjusted Gross Income (MAGI). This was a change instituted by the Affordable Care Act (ACA) to standardize eligibility.5 6.1.1 Calculating MAGI

MAGI is calculated as Adjusted Gross Income (AGI) from the tax return, plus:

-

Untaxed foreign income.

-

Non-taxable Social Security benefits.

-

Tax-exempt interest.17 6.1.7 The ROC Interaction

Crucially, Return of Capital (ROC) distributions are excluded from the definition of MAGI. Because ROC is considered a return of principal rather than income, it does not appear in AGI and is not added back. -

The Loophole: An investor under 65 could theoretically receive USD 114,000/year in STRC distributions (characterized as ROC), live a comfortable lifestyle, and report a MAGI of USD2.

-

Eligibility Thresholds: For a household of two, the income limit for MAGI Medi-Cal (138% of the Federal Poverty Level) is approximately USD 29,187 (projected for 2026 based on 2025 data).18 With a MAGI of USD2, the household qualifies for free, full-scope Medi-Cal coverage with no premiums, no deductibles, and no copays.19 6.1.4 Absence of Asset Test

For the MAGI population (under 65), there is no asset test.5 The state does not ask about bank accounts, stock portfolios, or cash on hand. Eligibility is strictly an income test. This allows the “California Arbitrage” practitioner to hold USD1 million in STRC stock without jeopardizing their health coverage.

4.7 The 2026 Asset Test Reinstatement (Age 65+ and Non-MAGI)

The strategy faces a critical “cliff” once the practitioner reaches age 65 or if they qualify for Medi-Cal on the basis of disability (Non-MAGI Medi-Cal).6.7.1 The “Golden Era” (2024-2025)

From January1, 2024, to December 31, 2025, California experimented with a radical policy: the complete elimination of asset limits for all Medi-Cal programs, including those for the elderly and disabled.5 During this brief window, a 70-year-old with USD8 million in the bank could qualify for Medi-Cal nursing home coverage provided their income was low enough.6.7.7 The Reversal (January1, 2026)

Facing significant budget deficits, the Department of Health Care Services (DHCS) is reinstating the asset test for Non-MAGI populations effective January1, 2026.20

-

New Asset Limits: The limits return to the 2022 levels adjusted for inflation but remain restrictive compared to the “no limit” era. The limit is USD 130,000 for an individual and USD 195,000 for a couple, with an additional USD 65,02 for each additional family member.20

-

Countable Assets: The test includes cash, bank accounts, investment accounts (stocks, bonds), and second vehicles. The primary residence (if inhabited) and one vehicle remain exempt.246.7.4 Strategic Implication for the Case Study

This regulatory change creates a bifurcation in the strategy’s viability: -

Under 65: The strategy works. The asset test does not apply to the MAGI population.

-

Over 65: The strategy fails. An individual holding USD1,02,02 in STRC stock would essentially be disqualified from Medi-Cal on January1, 2026, because their assets (USD1 million) vastly exceed the limit (USD 130k/USD 195k). They would be required to “spend down” their assets to regain eligibility.25

Therefore, the “Live Free” strategy using STRC is essentially an early retirement bridge strategy viable only for those under 65. Upon turning 65, the practitioner must transition to Medicare (which has premiums) and will lose full Medi-Cal eligibility unless they impoverish themselves or engage in complex estate planning (e.g., irrevocable trusts), which would strip them of access to their capital.

4.4 Estate Recovery and Probate Avoidance

A lingering fear for Medi-Cal recipients is the state’s Estate Recovery Program, which seeks repayment for services rendered from the assets of a deceased beneficiary.6.4.1 Scope of Recovery

For beneficiaries who die after January1, 2018, recovery is limited to payments made for nursing facility services, home and community-based services, and related hospital and prescription drug services received when the beneficiary was an inpatient or receiving those specific services. It generally applies to beneficiaries aged 55 and older.266.4.7 The Probate Limitation

Crucially, California law limits estate recovery to assets that are part of the decedent’s probate estate.22 Assets that transfer outside of probate are generally exempt from recovery.

- Mitigation Strategy: To protect the STRC capital from potential recovery claims (should the practitioner require long-term care services while on Medi-Cal), the assets must be held in a vehicle that avoids probate. The most common tool is a Revocable Living Trust. Assets titled in the name of the trust pass directly to beneficiaries upon death, bypassing probate and thus—under current California rules—bypassing Medi-Cal estate recovery.28

5. The Housing Strategy: Arbitraging Rents vs. Ownership Costs

The final component of the strategy is the conversion of the “freed” capital into shelter. The premise is that in many California markets, the cost to rent a luxury home is significantly lower than the cost to own it, particularly when factoring in the opportunity cost of equity.

5.1 The Financial Logic of Renting

Owning a home in California involves high carrying costs. A USD1.7 million home (a typical suburban 4-bedroom) incurs:

- Property Tax (~1.1%): USD3,200/year (USD1,100/mo).

- Insurance: USD7,500/year (USD 208/mo) - and rising rapidly due to wildfire risk.

- Maintenance (1%): USD15,000/year (USD1,000/mo).

- Cost of Equity: USD1.7 million invested at 5% risk-free = USD 60,000/year (USD8,000/mo).

By selling, the practitioner eliminates the tax, insurance, and maintenance liabilities. By investing the proceeds at 11% (STRC), the USD1.7 million generates USD 132,000/year (USD12,000/mo). If the practitioner can rent a comparable home for less than the yield, they create a surplus.

5.7 Rental Market Analysis (2026)

To maximize the “free” lifestyle, the practitioner must target markets where rent-to-price ratios are favorable. The goal is a6,02 sq ft (or spacious 4-bedroom) home for under USD6,000/mo.8.7.1 Sacramento and Suburbs

The Sacramento region offers a compelling balance of amenities and value.

-

Inventory: Listing data shows numerous 4-bedroom homes in desirable suburbs like Natomas (95835) and Elk Grove (95758) renting for USD7,82 - USD4,52 per month.29

-

Lifestyle: Access to the Bay Area (2 hours) and Lake Tahoe (1.8 hours), with newer housing stock built post-202.

-

Arbitrage: Renting at USD4,200/mo leaves nearly USD10,000/mo in surplus cash flow from the STRC investment.8.7.7 Riverside and the Inland Empire

Riverside County provides expansive square footage and master-planned communities. -

Inventory: Data indicates 4-bedroom homes in Riverside (92508/Orangecrest, 92503) renting for USD4,62 - USD4,92 per month.31

-

Lifestyle: Large lots, pools, and proximity to Orange County/LA employment hubs (though the practitioner effectively does not need to commute).

-

Arbitrage: Slightly tighter margins than Sacramento, but still well within the USD13,166/mo income stream.8.7.4 Fresno and the Central Valley

For the ultimate financial surplus, the Central Valley offers luxury rentals at bargain prices. -

Inventory: In North Fresno (93720/93730), near the prestigious Clovis Unified School District, 4-bedroom homes rent for USD7,72 - USD4,22 per month.33

-

Lifestyle: High-end suburban living with significantly lower congestion.

-

Arbitrage: Renting here maximizes disposable income, leaving over USD10,000/mo for travel, leisure, or reinvestment.8.7.6 The Coastal Barrier

The strategy hits a wall in coastal zones. Renting a 4-bedroom home in La Jolla, Santa Monica, or Newport Beach generally costs USD9,02 to USD20,000+ per month.35 This exceeds the projected STRC income, making the strategy unviable in these specific zip codes unless the practitioner has significantly more capital than the average Section 121 limit allows.

5.4 Inflation Risk in Renting

Unlike a fixed-rate mortgage, rent is not fixed. California has statewide rent control (AB 1482), generally capping increases at 5% plus CPI (up to 10%). However, single-family homes owned by individuals (not REITs/corporations) are often exempt from this cap.

- Risk: If rents rise by 5% annually for a decade, a USD4,52 rent becomes USD8,72. If the STRC dividend remains flat (or is cut), the practitioner’s discretionary income collapses. The strategy lacks the inflation hedge inherent in homeownership.

6. Risk Architecture: The “Widowmaker” Analysis

While the “California Arbitrage” is mathematically elegant, it creates a fragility in the household’s financial foundation. It replaces diversified assets with concentrated credit risk.

6.1 Concentration and Counterparty Risk

The most glaring risk is the lack of diversification. Placing the entirety of one’s net worth (derived from the home sale) into a single security (STRC) exposes the practitioner to total ruin if Strategy Inc. defaults.

- Credit Rating: As noted, S&P rates the company ‘B-’. Historical default rates for B-rated issuers over a 10-year period are significant (often exceeding 20-30%).

- Bitcoin Dependence: If Bitcoin crashes to USD14,02 or faces an existential regulatory ban, Strategy Inc.’s balance sheet would likely be impaired. While they might not default on bonds immediately, they could suspend preferred dividends to preserve cash. A suspension means zero income for the practitioner, who still has a lease obligation.

6.7 The “Rule Change” Risk

The strategy relies on a specific confluence of tax and welfare rules.

- IRS Recharacterization: If the IRS determines that Strategy Inc.’s distributions should be taxed as dividends rather than ROC (perhaps due to legislative changes closing the crypto-treasury loophole), the practitioner would suddenly have USD 114,02 in taxable income. This would disqualify them from MAGI Medi-Cal (threshold ~USD 29k), forcing them onto an ACA exchange plan with potential premiums and out-of-pocket costs.17

- State Policy: California could seek federal waivers to impose asset tests on the MAGI population, or close the “probate only” loophole for estate recovery, putting the trust assets at risk.

6.4 The Age Trap

The 2026 reinstatement of the asset test for seniors creates a “trap door.” A practitioner executing this strategy at age 55 enjoys14 years of “free” living. However, the day they turn 65, they become subject to the Non-MAGI asset test.

- Scenario: At age 65, they have USD1 million in STRC stock. The asset limit is USD 130,02. They are immediately kicked off Medi-Cal.

- Consequence: They must transition to Medicare (which has premiums for Part B and D). If they need long-term care (nursing home), they are ineligible for Medi-Cal coverage until they spend down their USD1 million to USD 130k. This destroys the legacy they hoped to preserve.

6.6 The STRC strategy is a depleting asset bridge, not a perpetual wealth machine.

The Zero Basis Clock (The \$\sim13 USD-Year Horizon): An 11% yield on a USD1,02,02 investment (USD 114,000/year) reduces the cost basis to zero in \$\sim13.1 USD years. Around Year14, distributions become taxable Capital Gains instead of tax-deferred Return of Capital. Federally, the income may remain 0% tax for a couple (due to the capital gains preference). However, California has no capital gains preference, resulting in a sudden 4-6% state income tax (\$\sim\$USD8,000–USD9,000/year) on the USD 114,02.

The Reskilling Imperative: This strategy requires a “reskilling window” to hedge against risks. Inflation (at 3%) will erode the USD 114,02 to \$\sim\$USD 80,02 in purchasing power by 2036. Additionally, at age 65, the loss of full Medi-Cal and the new fixed cost of Medicare Part B and D premiums (over USD8,000/year for a couple) will further deplete the STRC income.

7. Conclusion

The “Living Free in California” case study represents the apex of aggressive personal finance engineering. It successfully identifies and exploits the seams between the tax code (Section 121, ROC), the healthcare system (ACA/MAGI), and the capital markets (High-Yield Crypto Derivatives).

For a household under age 65, willing to accept the volatility of a Bitcoin-linked treasury and the flexibility of renting in inland markets, the strategy theoretically delivers a lifestyle of abundance (six-figure spending power, zero tax, free healthcare). It effectively socializes the cost of healthcare while privatizing the yield of high-risk assets.

However, the strategy is not a passive retirement plan; it is an actively managed, high-beta hedge fund trade. It carries existential risks—specifically the creditworthiness of Strategy Inc. and the regulatory “cliff” at age 65—that make it unsuitable for the risk-averse. The reinstatement of the asset test in 2026 serves as a stark reminder that the government’s largesse has boundaries, and for the elderly, the “free lunch” is officially over.

Disclaimer: This report is for informational purposes only and does not constitute legal, tax, financial, or medical advice. The strategies discussed involve significant risks, including the potential for total loss of principal and loss of health coverage. Strategy Inc. (STRC) is a highly volatile security. Tax laws and Medi-Cal eligibility rules are subject to change. Readers should consult with qualified professionals before making any financial decisions.

Appendix: Selected Data Tables

Table 1: Capital Gains Tax Comparison (2026 Projections)

Impact of Section 121 Exclusion on a USD 52,02 Gain

| Scenario | Federal Tax (15-20%) | NIIT (3.8%) | CA State Tax (~9.3-14.3%) | Total Tax Liability | Net Proceeds |

|---|---|---|---|---|---|

| No Exclusion | ~USD 75,02 - USD 12,02 | ~USD16,02 | ~USD 46,52 - USD 66,52 | ~USD 140,52 - USD 185,500 | ~USD 35,52 |

| With Sec 121 | USD2 | USD2 | USD2 | USD 0 | USD 52,000 |

| Advantage | +USD 185,500 |

Table 2: 2026 Medi-Cal Asset Limits (Non-MAGI)

Effective Jan1, 2026, for Aged (65+), Blind, and Disabled

| Household Size | Asset Limit (Countable Assets) |

|---|---|

| 1 Person | USD 130,02 |

| 2 People | USD 195,02 |

| Each Add’l Member | +USD 65,02 |

| Exempt Assets | Primary Residence (if inhabited), One Vehicle, Household Goods, IRAs in payout status. |

| Countable Assets | Cash, Checking/Savings, Stocks/Bonds (STRC), Second Vehicles, Vacation Homes. |

Source: 22

Table 3: Rental Market Arbitrage (4bd/3ba Homes)

Monthly Rent vs. STRC Monthly Yield (USD1 million Investment)

| City/Area | Approx. Rent (2026 Est.) | STRC Yield (@ 11%) | Monthly Surplus |

|---|---|---|---|

| Fresno (North) | USD7,92 | USD13,166 | +USD10,266 |

| Sacramento (Natomas) | USD4,22 | USD13,166 | +USD8,966 |

| Riverside (Orangecrest) | USD4,82 | USD13,166 | +USD8,366 |

| La Jolla | USD11,52 | USD13,166 | +USD 666 |

Source: 213

Tips and Donations

If you enjoyed this deep dive, consider supporting the project with a tip in Sats. It’s a simple, global way to support independent research.

To send Sats, you’ll need a lightning wallet.

References

-

What is the long-term capital gains tax? Here are the rates for 2025-2026 - Bankrate, accessed January 12, 2026, https://www.bankrate.com/investing/long-term-capital-gains-tax/ ↩ ↩2 ↩3 ↩4 ↩5 ↩6 ↩7 ↩8 ↩9 ↩10 ↩11 ↩12 ↩13 ↩14 ↩15 ↩16 ↩17 ↩18 ↩19 ↩20 ↩21 ↩22 ↩23 ↩24 ↩25 ↩26 ↩27 ↩28 ↩29 ↩30 ↩31 ↩32 ↩33 ↩34 ↩35 ↩36 ↩37 ↩38 ↩39 ↩40

-

Houses For Rent in San Diego CA - 1495 Homes | Zillow, accessed January 12, 2026, https://www.zillow.com/san-diego-ca/rent-houses/ ↩ ↩2 ↩3 ↩4 ↩5 ↩6 ↩7 ↩8 ↩9 ↩10 ↩11 ↩12 ↩13 ↩14 ↩15 ↩16 ↩17 ↩18 ↩19 ↩20 ↩21 ↩22 ↩23 ↩24 ↩25 ↩26 ↩27 ↩28 ↩29 ↩30 ↩31 ↩32 ↩33 ↩34 ↩35 ↩36 ↩37 ↩38 ↩39 ↩40 ↩41 ↩42 ↩43 ↩44 ↩45 ↩46 ↩47 ↩48 ↩49 ↩50 ↩51 ↩52 ↩53 ↩54 ↩55 ↩56 ↩57 ↩58 ↩59 ↩60 ↩61 ↩62 ↩63 ↩64

-

Nicholas Crypto Income ETF (BLOX) Company Sentiment and Research Comments | Seeking Alpha, accessed January 12, 2026, https://seekingalpha.com/symbol/BLOX/comments ↩ ↩2 ↩3 ↩4 ↩5

-

Tax laws 2025: Tax brackets and deductions - U.S. Bank, accessed January 12, 2026, https://www.usbank.com/wealth-management/financial-perspectives/financial-planning/tax-brackets.html ↩ ↩2 ↩3 ↩4 ↩5 ↩6 ↩7 ↩8 ↩9 ↩10 ↩11 ↩12 ↩13 ↩14 ↩15 ↩16 ↩17 ↩18 ↩19 ↩20 ↩21 ↩22 ↩23 ↩24 ↩25 ↩26 ↩27 ↩28 ↩29

-

Medi-Cal Considers Income, Not Assets, of Enrollees - California Health Care Foundation, accessed January 12, 2026, https://www.chcf.org/resource/medi-cal-considers-income-not-assets-enrollees/ ↩ ↩2 ↩3 ↩4 ↩5

-

Capital Gains Tax Rates 2025 and 2026: What You Need to Know - Kiplinger, accessed January 12, 2026, https://www.kiplinger.com/taxes/capital-gains-tax/602224/capital-gains-tax-rates ↩ ↩2 ↩3 ↩4 ↩5 ↩6 ↩7 ↩8 ↩9 ↩10 ↩11 ↩12 ↩13

-

2025 and 2026 capital gains tax rates - Fidelity Investments, accessed January 12, 2026, https://www.fidelity.com/learning-center/smart-money/capital-gains-tax-rates ↩ ↩2 ↩3 ↩4 ↩5 ↩6 ↩7 ↩8 ↩9 ↩10 ↩11 ↩12 ↩13 ↩14 ↩15 ↩16 ↩17 ↩18 ↩19 ↩20 ↩21 ↩22 ↩23 ↩24 ↩25 ↩26 ↩27 ↩28 ↩29

-

Strategy Inc Assigned ‘B-’ Issuer Credit Rating; Outlook Stable - S&P Global, accessed January 12, 2026, https://www.spglobal.com/ratings/en/regulatory/article/-/view/type/HTML/id/3466223 ↩ ↩2 ↩3 ↩4 ↩5 ↩6 ↩7 ↩8 ↩9 ↩10 ↩11 ↩12 ↩13 ↩14 ↩15 ↩16 ↩17

-

Strategy Inc Class A (MSTR) Stock Price & News - Google Finance, accessed January 12, 2026, https://www.google.com/finance/quote/MSTR:NASDAQ ↩ ↩2 ↩3

-

MicroStrategy - Wikipedia, accessed January 12, 2026, https://en.wikipedia.org/wiki/MicroStrategy ↩ ↩2 ↩3 ↩4

-

424B5 - SEC.gov, accessed January 12, 2026, https://www.sec.gov/Archives/edgar/data/1050446/000119312525263719/d922690d424b5.htm ↩ ↩2 ↩3

-

Strategy Announces Third Quarter 2025 Financial Results, accessed January 12, 2026, https://www.strategy.com/press/strategy-announces-third-quarter-2025-financial-results_10-30-2025 ↩ ↩2 ↩3

-

MicroStrategy Incorporated Variable Rate Series A Perpetual Stretch Preferred Stock Stock Price: Quote, Forecast, Splits & News (STRC) - Perplexity, accessed January 12, 2026, https://www.perplexity.ai/finance/STRC?ref=worldaviationmedia.com ↩ ↩2 ↩3 ↩4 ↩5 ↩6 ↩7 ↩8 ↩9 ↩10

-

STRC Information - Strategy, accessed January 12, 2026, https://www.strategy.com/stretch ↩ ↩2 ↩3 ↩4 ↩5 ↩6 ↩7 ↩8 ↩9 ↩10

-

MSTR 8-K: STRC monthly dividend USD 0.875; rate now 10.50% - Stock Titan, accessed January 12, 2026, https://www.stocktitan.net/sec-filings/MSTR/8-k-strategy-inc-reports-material-event-5c56cfac3cc3.html ↩ ↩2

-

Medi-Cal’s Asset Limit is Now Eliminated - California Health Advocates, accessed January 12, 2026, https://cahealthadvocates.org/medi-cals-asset-limit-is-now-eliminated/ ↩ ↩2

-

Income Definitions for Marketplace and Medicaid Coverage - Beyond the Basics, accessed January 12, 2026, https://www.healthreformbeyondthebasics.org/key-facts-income-definitions-for-marketplace-and-medicaid-coverage/ ↩ ↩2

-

Qualify | Medi-Cal - DHCS - CA.gov, accessed January 12, 2026, https://www.dhcs.ca.gov/Medi-Cal/Pages/eligibility-chart.aspx ↩ ↩2

-

MAGI Medi-Cal Fact Sheet - Santa Cruz County Human Services, accessed January 12, 2026, https://santacruzhumanservices.org/Portals/0/Factsheets/English/Modified-Adjusted-Gross-Income-Medi-Cal-Fact-Sheet%20(2-28-2023).pdf?ver=E3vUpwvusYJ_w9zL81Lalg%3D%3D ↩

-

California Medicaid (Medi-Cal) Eligibility: 2026 Income & Asset Limits, accessed January 12, 2026, https://www.medicaidplanningassistance.org/medicaid-eligibility-california/ ↩ ↩2 ↩3