Mechanics of the Invincible Dollar

Date: February 26, 2026

Subject: Macroeconomics and International Finance

Abstract

This paper examines the structural foundations of the United States Dollar (USD) as the global reserve currency, moving beyond the historical context of the Bretton Woods Accord. It argues that reserve status is fundamentally tied to the “Triffin Dilemma [5]”—the necessity of the issuing nation to run persistent trade deficits to provide global liquidity. Furthermore, this paper distinguishes between trade deficits as a structural requirement and tariffs as a microeconomic policy tool. Finally, it analyzes the “Impossible Dream” of the Chinese Yuan (RMB), which seeks reserve status while maintaining export dominance and capital controls, two conditions that are mathematically and economically at odds.

I. Introduction: Beyond Bretton Woods

While the 1944 Bretton Woods Accord established the USD as the world’s primary anchor, the collapse of the gold standard in 1971 transitioned the dollar into a “pure” fiat reserve system. Modern USD hegemony is not maintained by treaty, but by the structural architecture of global trade. To understand this, one must decouple the political rhetoric regarding trade deficits from the functional necessity of currency exportation [2].

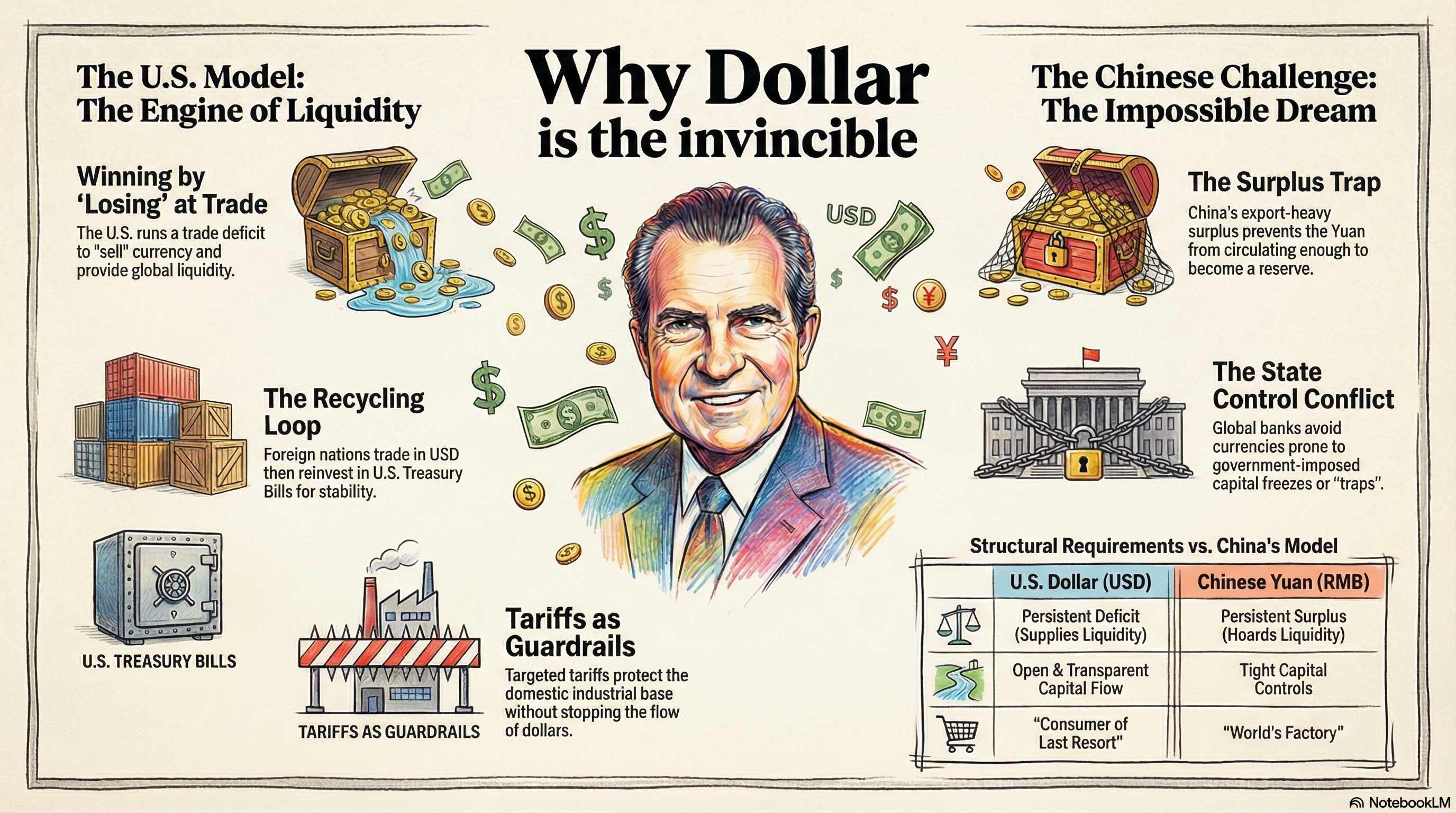

II. The Triffin Dilemma and the Necessity of Deficits

The primary engine of USD supremacy is the trade deficit. Under the Triffin Dilemma, the home country of a reserve currency must provide the rest of the world with a steady supply of its currency to facilitate global trade.

- Liquidity Provision: If the U.S. ran a trade surplus, it would be “sucking” dollars out of the global economy, leading to a liquidity crunch and a contraction in world trade.

- The Recycling Mechanism: Foreign nations accumulate USD through trade surpluses with the U.S. and subsequently “recycle” these dollars into U.S. Treasury Bills. This creates a deep, liquid market for U.S. sovereign debt, lowering domestic borrowing costs [3].

III. Tariffs as Policy vs. Deficits as Structure

A common fallacy in economic discourse is the mixing of tariffs and trade deficits.

- The Trade Deficit is a macroeconomic outcome of the U.S. role as the global consumer of last resort and the global provider of safe assets.

- Tariffs are microeconomic instruments. Their primary utility is not to “fix” the aggregate trade deficit—which is driven by national savings and investment balances—but to protect specific domestic sectors or modify the behavior of trading partners [1].

Using tariffs to eliminate a trade deficit is often counterproductive; a reduction in imports typically leads to a stronger dollar, which in turn hurts exports, leaving the total deficit largely unchanged while increasing costs for domestic consumers.

IV. China’s “Impossible Dream”

China’s ambition to internationalize the Yuan (RMB) faces a fundamental paradox. Beijing seeks the benefits of a reserve currency—seigniorage, lower borrowing costs, and geopolitical leverage—without accepting the requisite structural changes.

- Export Dominance vs. Currency Supply: China’s economic model is predicated on being the “World’s Factory.” Maintaining a trade surplus is incompatible with providing the world with Yuan liquidity.

- The Capital Account Paradox: A reserve currency must be “free and clear.” China’s use of capital controls to maintain domestic stability prevents the RMB from becoming a true safe-haven asset. Central banks are hesitant to hold reserves that cannot be liquidated or moved during a crisis due to state intervention [4].

- The Governance Gap: Unlike the USD, which is backed by a transparent legal system and an independent central bank, the RMB remains subject to the discretionary policy shifts of the CCP, creating a “risk premium” that hinders global adoption.

V. Conclusion

The USD remains the global reserve currency because the United States is the only major economy willing to accept the “tax” of a persistent trade deficit in exchange for financial hegemony. China’s attempt to achieve reserve status while maintaining export dominance and capital restrictions represents an “Impossible Dream.” Until a nation is willing to open its capital markets and run a trade deficit to supply the world with liquidity, the USD’s structural position remains unchallenged by traditional nation-state competitors.

References

-

Bown, C. P. (2021). “Anatomy of a Flop: Why Trump’s US-China Phase One Trade Deal Fell Short.” Peterson Institute for International Economics. https://www.piie.com/publications/policy-briefs/anatomy-flop-why-trumps-us-china-phase-one-trade-deal-fell-short

-

Eichengreen, B. (2011). “Exorbitant Privilege: The Rise and Fall of the Dollar and the Future of the International Monetary System.” Oxford University Press. https://global.oup.com/academic/product/exorbitant-privilege-9780199753765

-

Pettis, M. (2011). “The Volatility Machine: Emerging Economies and the Threat of Financial Collapse.” Oxford University Press. https://global.oup.com/academic/product/the-volatility-machine-9780199763740

-

Prasad, E. S. (2016). “Gaining Ground: The Rise of the Renminbi.” Brookings Institution Press. https://www.brookings.edu/book/gaining-ground/

-

Triffin, R. (1960). “Gold and the Dollar Crisis: The Future of Convertibility.” Yale University Press. https://research.stlouisfed.org/publications/review/1961/01/01/gold-and-the-dollar-crisis-the-future-of-convertibility/

Tips and Donations

If you enjoyed this deep dive, consider supporting the project with a tip in Sats. It’s a simple, global way to support independent research.

To send Sats, you’ll need a lightning wallet.