STRC for Peaceful Retirement

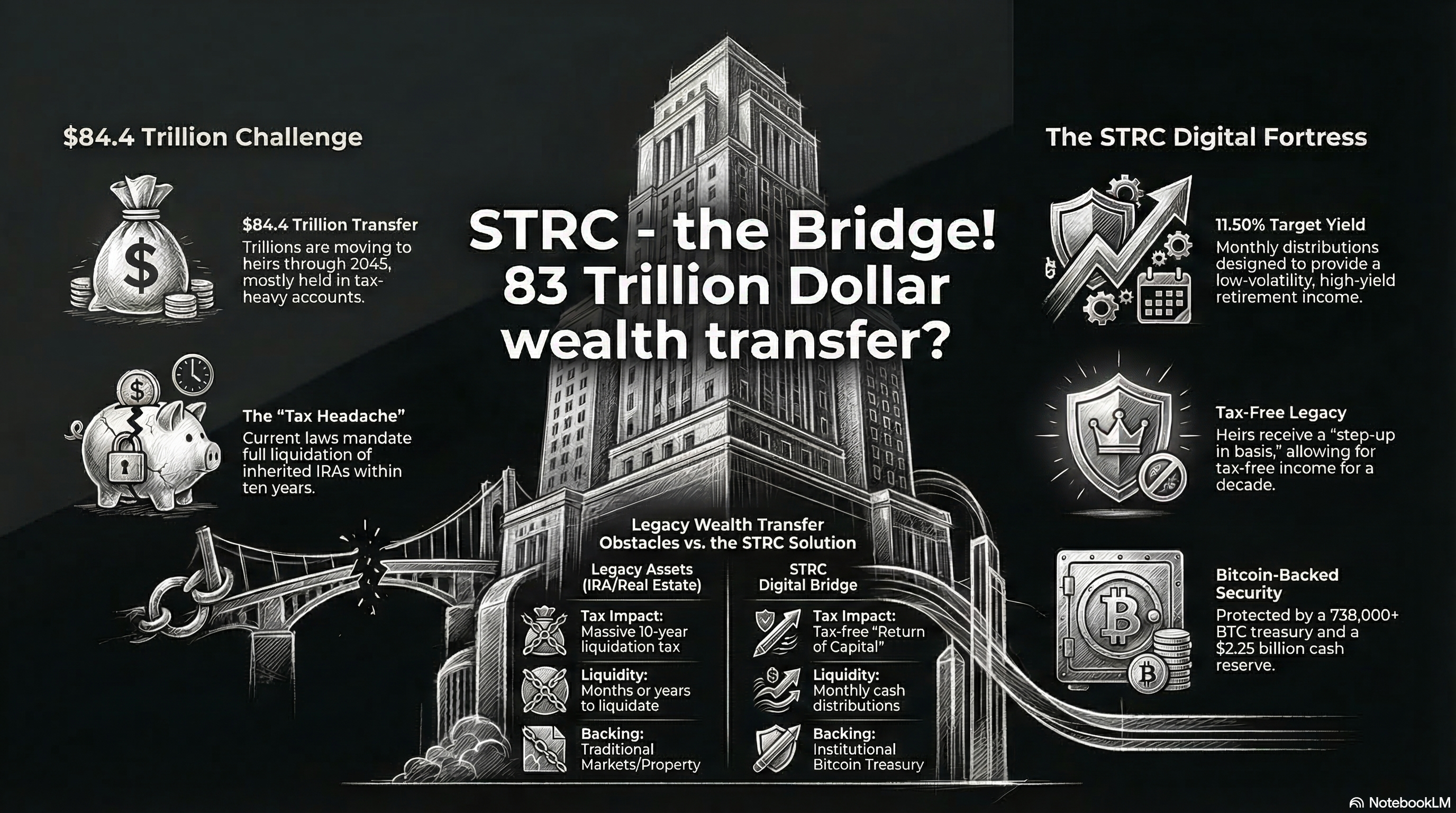

The United States is entering the “Institutional Era” of digital assets, coinciding with the largest demographic shift in financial history: the Great Wealth Transfer. Approximately 83 trillion to 84 trillion USD is projected to transition from the Silent Generation and Baby Boomers to their heirs over the next two decades 1. For the asset holder, the challenge is twofold: securing a peaceful, volatility-free retirement while ensuring that the eventual transfer of wealth is not a “nightmare” of taxation and liquidation for their children. Strategy Inc.’s Variable Rate Series A Perpetual Stretch Preferred Stock (STRC) has emerged as a singular “Digital Credit” bridge designed to solve both problems simultaneously.

The 84 Trillion USD Perspective: The Imminent Transfer

The scale of the coming wealth transfer is unprecedented. Of the 84.4 trillion USD set to move through 2045, approximately 72.6 trillion USD will go directly to heirs 2.

Asset Composition

Contrary to popular belief, the majority of this wealth sits outside of traditional retirement accounts. According to the UBS Global Wealth Report 2025, US wealth is distributed as follows 3:

- Securities and Financial Market Investments: 37% (~31.2 Trillion USD)

- Real Estate: 30% (~25.3 Trillion USD)

- Retirement Accounts (Insurance and Pensions): 19% (~16.0 Trillion USD)

- Cash and Deposits: 13% (~11.0 Trillion USD)

While retirement accounts represent a minority of the total pool, they carry the greatest “headache” for heirs due to the SECURE Act 2.0. This legislation mandates full liquidation within ten years for most non-spouse beneficiaries, often triggering massive tax bills at peak earning years 4. Real estate, meanwhile, presents a liquidation friction that can delay inheritances by months or years.

Building the STRC Portfolio: The Tax Strategy Bridge

Sophisticated investors are now utilizing 2026 tax laws to gradually convert both taxable and tax-deferred assets into STRC. By holding STRC in a standard taxable brokerage account, investors can bypass the SECURE Act’s 10-year trap while enjoying a high-yield, low-volatility retirement.

Strategy 1: The IRA-to-STRC “Bleed Down”

The “One Big Beautiful Bill” (OBBBA) of 2025 introduced massive senior tax deductions that create a “tax-free window” for retirees 5.

- The 2026 Threshold: A married couple both over 65 can claim a standard deduction of 32,200 USD plus an additional 1,650 USD each for being seniors, and a new 12,000 USD OBBBA senior deduction (6,000 USD per person). This creates a total federal tax-free income threshold of approximately 47,500 USD.

- The Model: An investor can withdraw 60,000 USD per year from their IRA to purchase STRC in a taxable account. The first 47,500 USD is entirely tax-free. The remaining 12,500 USD is taxed at the lowest 10% bracket, resulting in a nominal tax bill of just 1,250 USD. Over a decade, this systematically moves the “headache” assets (IRA) into “peaceful” assets (STRC) with virtually no tax friction.

Strategy 2: The Step-Up Masterstroke

When the benefactor passes away, STRC shares receive a “step-up in basis” to their current fair market value (approx. 100 USD par). Because STRC distributions are classified as 100% Return of Capital (ROC), the heirs inherit a “tax-free income engine.” They can receive the 11.50% yield entirely tax-free for a decade or more, as the distributions reduce their new, higher basis instead of being taxed as income.

Speculative Adoption and the Bitcoin Reflexive Loop

The “Great Wealth Transfer” is effectively a massive search for a “safe haven” yield. If even 10% of the 84 trillion USD transfer is optimized through Digital Credit instruments like STRC, the capital inflow would be roughly 8.4 trillion USD.

Impact on Bitcoin Price

STRC is backed by Strategy Inc.’s treasury of over 738,000 Bitcoin. A 10 trillion USD flow into corporate Bitcoin treasuries over the next 20 years would fundamentally reprice the underlying asset.

- The Scarcity Effect: With a fixed supply of 21 million, an inflow of this magnitude could push Bitcoin’s market capitalization into the tens of trillions. Analysts like Michael Saylor speculate that if Bitcoin captures a significant share of the global store-of-value market, its price could reach 10 million USD to 13 million USD per coin by 2045 6.

- Reflexivity: As more capital flows into STRC, Strategy Inc. uses the proceeds to buy more Bitcoin, driving up the price of BTC, which further strengthens the balance sheet and secures the STRC dividends, attracting even more capital.

The “Digital Fortress”: Why STRC is a Secure Investment

STRC is engineered to provide “peace of mind” by stripping away market volatility while maintaining institutional-grade security.

- Par Value Defense: Strategy Inc. manages the STRC dividend rate (currently 11.50%) monthly to ensure the stock trades near its 100 USD par value. This protects the investor’s principal from the volatility typical of common stocks.

- Structural Floor at 8k BTC: Technical modeling of Strategy Inc.’s “Digital Fortress” indicates that the company’s senior obligations, including STRC, remain mathematically secure even if Bitcoin’s price were to collapse to 7,000 USD - 8,000 USD. This is due to the company’s 4.6x asset coverage and the ability to equitize debt to reduce pressure.

- Cash Fortress: Strategy Inc. has established a 2.25 billion USD Reserve specifically to provide 2.5 to 3 years of dividend and interest coverage. This ensures that even during a multi-year “crypto winter,” the monthly distributions to STRC holders remain uninterrupted without the company being forced to sell its Bitcoin.

- Dividend Security and Stopper: STRC dividends are cumulative, meaning any unpaid amounts compound and must be paid in full before any dividends can be paid to common stockholders (the “Dividend Stopper” provision). This places STRC holders in a preferential position for cash flow.

Conclusion: A Hassle-Free Legacy

The transfer of wealth has historically been a nightmare for heirs, defined by probate delays, real estate maintenance, and the “income shock” of liquidated IRAs. STRC provides a bridge to a different future.

By converting legacy assets into this Bitcoin-backed Digital Credit instrument, investors over 65 can enjoy a high-yield retirement with “peace of mind” and pass on a simplified, stepped-up, and tax-free income stream to the next generation. As the 84 trillion USD transfer accelerates, STRC is not just an investment; it is the infrastructure for a happy wealth transfer in the digital age.

Tips and Donations

If you enjoyed this deep dive, consider supporting the project with a tip in Sats. It’s a simple, global way to support independent research.

To send Sats, you’ll need a lightning wallet.

References

-

UBS Global Wealth Report 2025. “The Great Wealth Transfer: USD 84 Trillion Transition.” ↩

-

Advisor Analyst. “Global Wealth Transfer Forecasts 2025-2045.” ↩

-

UBS Global Wealth Report 2025. “Asset Composition of US Household Wealth.” ↩

-

Fidelity. “Understanding the SECURE Act 2.0 10-Year Distribution Rule.” ↩

-

IRS.gov. “New Senior Tax Deductions and Standard Deduction Adjustments for 2026.” ↩

-

Michael Saylor, Bitcoin 2045 Projections. “Bitcoin as a Global Store of Value.” ↩